Alibaba’s $100 Billion AI Target Has a Timing Problem

Alibaba’s AI demand looks real. The harder question is whether cloud can scale before commerce stops funding the transition.

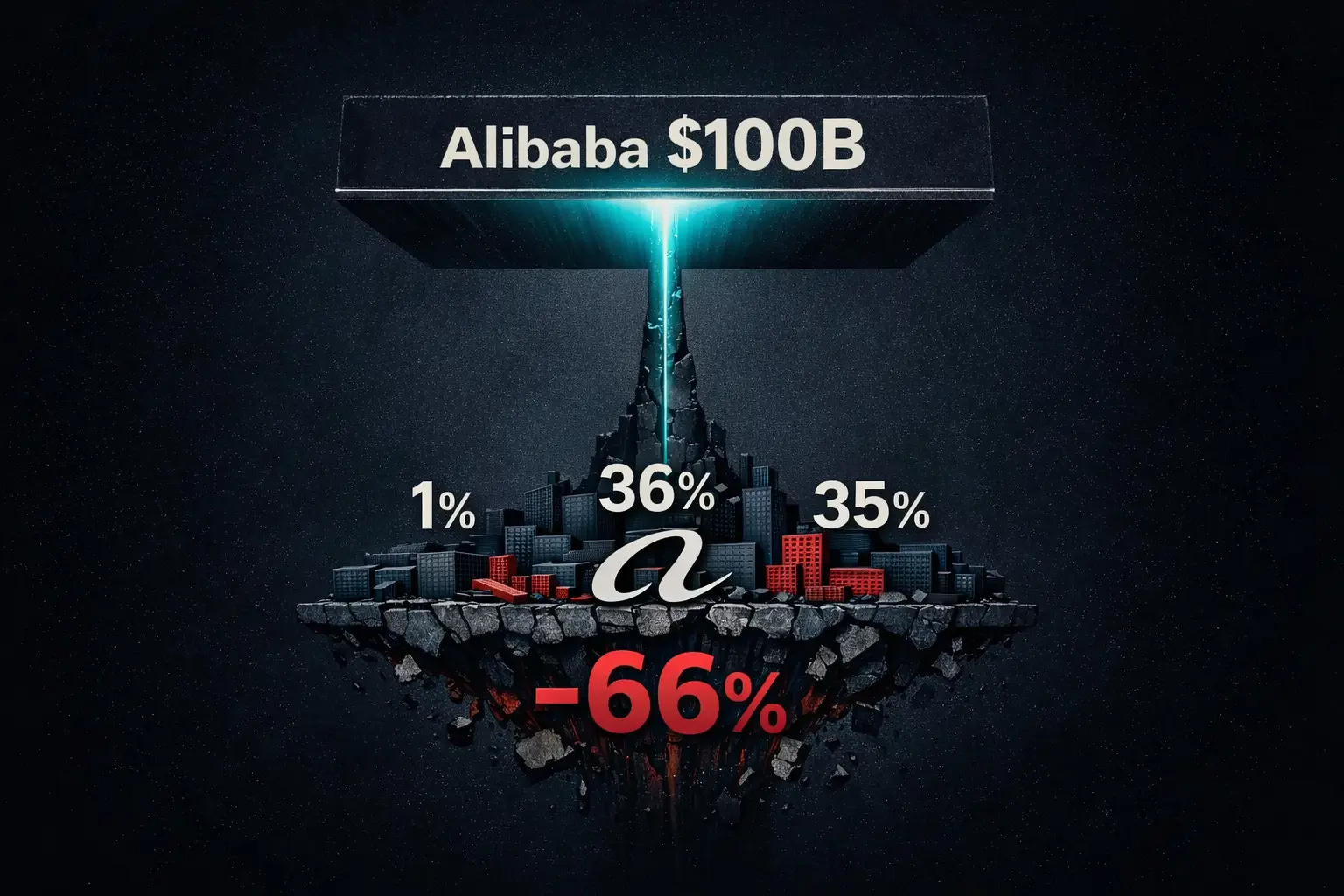

On the evening of March 19, Alibaba CEO Eddie Wu delivered a number that overshadowed everything else on the quarterly earnings call: combined cloud and AI external revenue, including model-as-a-service, will exceed $100 billion within five years. That would push this segment of Alibaba’s business to roughly the same scale as AWS, which generated $107.6 billion in 2024, and would account for well over half of Alibaba’s current total annual revenue.

The timing made the promise harder to absorb. The same earnings report showed a 66% drop in net income, a 57% decline in adjusted EBITA, and free cash flow down 71% year over year. Customer management revenue (CMR), the core metric of Alibaba’s e-commerce advertising engine, grew 1%. Alibaba’s US-listed shares fell more than 7% after the results. Together with Tencent, whose own earnings disappointed the same week, Chinese tech’s two largest companies shed $66 billion in combined market value within 24 hours.

Wu was asking investors to look past the worst profit quarter in years and focus on a horizon where the company’s primary revenue source shifts from e-commerce advertising to AI infrastructure. The market, at least initially, declined the invitation.

Whether the market was right depends on questions the earnings data can partially answer. This piece stress-tests the $100 billion target against what the numbers show, what industry dynamics support, and where the assumptions break.

Two Companies in One Balance Sheet

Alibaba’s quarterly results read like dispatches from two different businesses sharing a single ticker symbol.

The consumption side of the company is under pressure on nearly every front. China’s online retail sales grew around 2% in the December quarter, weighed by fading government subsidy effects and a late Lunar New Year that shifted spending into the March quarter. Within that weak environment, Alibaba’s e-commerce performance was softer still. A 0.6% software service fee introduced in September 2024, which had lifted take rates in prior quarters, completed its base period comparison, removing a tailwind. Quick Commerce (the food delivery and instant retail business rebranded as “Taobao Flash Shopping”) generated RMB 20.8 billion in revenue, up 56% year over year, but at a steep cost. The China E-commerce Group’s adjusted EBITA fell 43% to RMB 34.6 billion. According to estimates by Dolphin Research, a Chinese equity research firm, the Quick Commerce segment’s quarterly operating loss reached approximately RMB 25 billion, near the upper end of market expectations.

The other side of the ledger told a different story. Cloud Intelligence Group revenue grew 36% to RMB 43.3 billion. Revenue from external customers (excluding Alibaba’s own subsidiaries) accelerated to 35% growth, up from 29% the prior quarter. AI-related product revenue sustained triple-digit year-over-year growth for the tenth consecutive quarter. On Bailian, Alibaba’s model-as-a-service platform where developers access AI models through APIs, public model token consumption increased sixfold in three months.

Cloud adjusted EBITA reached RMB 3.9 billion, up 25%, with margins steady at 9%. In a quarter where nearly everything else deteriorated, cloud delivered both faster revenue growth and higher profits.

The cost of sustaining both realities was visible across the income statement. Sales and marketing expenses rose from roughly 15% to roughly 25% of revenue year over year, driven by Quick Commerce subsidies and user acquisition spending on consumer AI apps. Capital expenditure reached RMB 29.0 billion. The “All Others” segment, which houses Qwen model development and various AI investments, posted an adjusted EBITA loss of RMB 9.8 billion, tripling from the prior year.

The $100 Billion Equation

Alibaba Cloud’s cumulative external revenue for fiscal year 2026 (ending February) surpassed RMB 100 billion, roughly $14 billion. Wu’s target encompasses a broader scope: combined cloud and AI external revenue including MaaS, which likely spans both the Cloud Intelligence Group and the newly formed Alibaba Token Hub (ATH) business group. Reaching $100 billion annually within five years implies a compound annual growth rate above 40% from the current base.

That pace has a limited set of precedents. AWS grew from $17.5 billion in 2017 to $107.6 billion in 2024, compounding at approximately 29% annually, in a period before the agent-driven demand surge the industry is experiencing today. Microsoft’s Intelligent Cloud segment followed a comparable trajectory. Wu is promising significantly faster growth in a market that is smaller, more competitive, and constrained by US chip export controls that limit access to NVIDIA’s most advanced GPUs.

On the call, Wu outlined three engines he expects to power the trajectory.

First, model-as-a-service, centered on the Bailian platform and fueled by the explosive growth of AI agent workloads. Wu offered a claim worth examining closely: enterprises are increasingly treating token consumption as a production and R&D expense rather than an IT budget line item, effectively recategorizing AI compute as a core input alongside labor and materials. If accurate, this reframes the addressable market from the traditional 5% of corporate revenue allocated to IT toward a much larger slice of total operating costs.

Second, enterprise private deployment. Regulated industries and large companies will continue to need on-premises or hybrid cloud infrastructure for proprietary AI workloads that public APIs cannot serve. Each enterprise’s choices between public MaaS and private deployment will depend on the sensitivity of the use case, the specificity of the data, and the security requirements involved.

Third, traditional CPU-centric cloud, rebuilt for agents. This was the most underappreciated argument Wu made. Traditional cloud was designed for human IT engineers, a population that numbers perhaps 10 million in China. AI agents could eventually number in the billions. Each one requires CPU compute, databases, storage, and persistent memory. Transforming the existing cloud platform from serving human administrators to serving machine callers is, in Wu’s framing, an opportunity as large as AI-native workloads themselves.

These three engines are not equally likely to deliver on the same timeline:

MaaS is closest to producing visible revenue, with token consumption already surging and a pricing cycle working in its favor.

Enterprise private deployment offers steady demand but faces margin pressure from large-customer bargaining power and heavy customization requirements; if Alibaba chases volume through discounts on large contracts, this engine could add revenue while eroding profitability.

The agent-driven cloud transformation carries the longest time horizon and the highest uncertainty, because it depends on enterprise AI agent adoption reaching a scale that remains largely aspirational. The order in which these engines fire, and which ones stall, will determine whether the $100 billion figure lands as a forecast or a wish.

Continue reading with a paid subscription.